Client Alert – Mexico Rolls Out a Game-Changing Film & Audiovisual Tax Credit: What Producers, Streamers, and Investors Need to Know

Apr 2, 2026

WHY THIS MATTERS NOW

On 30 March 2026, Mexico published the long-awaited Lineamientos (Guidelines) implementing the Presidential Decree of 16 February 2026 that created a brand-new transferable income tax credit for film and audiovisual productions carried out in Mexican territory. This is not a revival of Mexico’s former EFICINE stimulus (Article 189 of the Income Tax Law), it is a different, more ambitious, and more flexible incentive designed to attract international productions, strengthen Mexico’s domestic supply chain, and create a secondary market for tax credit transfers.

The new Estímulo Fiscal a la Inversión en Cine y Audiovisual (“EFICA”) mechanism is now fully operational. Below, we provide an in-depth analysis of the program’s structure, the transfer mechanics that make it uniquely attractive, and the strategic considerations that media companies, streaming platforms, studios, and financial investors should evaluate.

THE INCENTIVE AT A GLANCE

The EFICA provides a tax credit of up to 30% of the total eligible cost of a film or audiovisual production project, including development, pre-production, production, post-production, and final delivery, provided those costs are incurred in Mexican territory and are deductible for income tax purposes.

Who Can Apply?

- Mexican-resident individuals and legal entities engaged in film or audiovisual production.

- Foreign residents with a permanent establishment in Mexico carrying out production activities.

- Foreign residents without a permanent establishment, provided they execute their project through a Mexican-resident production company under a documented contractual arrangement. This is a notable design choice: it explicitly opens the door to Hollywood studios and international streamers operating through local service producers without triggering PE risk.

Minimum Spend Thresholds

Practical insight: The MXN 5 million threshold for VFX and post-production processes is remarkably low, positioning Mexico as a viable nearshoring destination for post-production work that might otherwise go to Canada, the UK, or Eastern Europe. For streaming platforms already producing original content in Spanish, routing post-production through Mexico could unlock meaningful tax savings.

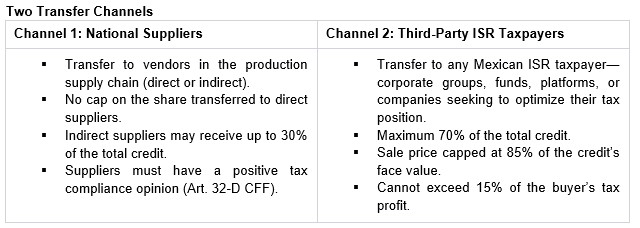

THE TRANSFER MECHANISM:

What truly sets EFICA apart from most international film incentives and certainly from Mexico’s legacy EFICINE is the ability to transfer the tax credit to third parties for consideration. This creates a secondary market for the credits and changes who benefits:

Relevant for investors: Channel 2 effectively creates a tax credit marketplace. A large Mexican corporate taxpayer with significant ISR liability can purchase EFICA credits at a discount (up to 85 cents on the peso) and apply them against its own income tax for provisional payments or the annual return. The producer, in turn, monetizes a credit it might not fully utilize. This is similar to the transferable tax credit models used in Georgia, New Jersey, and Louisiana in the United States, but with a distinct Mexican compliance overlay.

Critical anti-abuse guardrail: The Guidelines expressly prohibit re-transfer of the credit to additional third parties, including through mergers, spin-offs (escisión), or any other legal mechanism. Each credit is a one-hop transfer only.

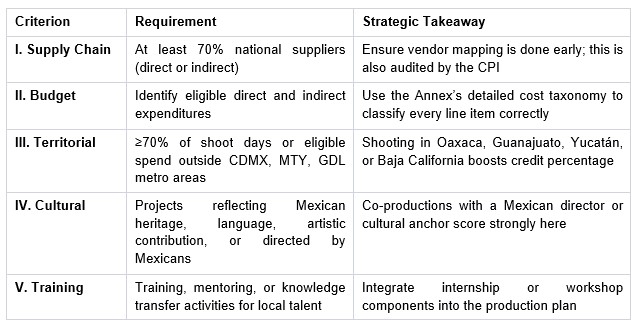

FIVE ELIGIBILITY CRITERIA: THE SCORING MATRIX

The Technical Committee evaluates projects against five criteria. Meeting criteria III, IV, and V unlocks the full 30% credit (otherwise, the Committee may award a lower percentage):

Practical insight: Criteria III, IV, and V create a deliberate policy incentive to decentralize production away from Mexico City, Monterrey, and Guadalajara, to invest in culturally significant content, and to develop local talent. Productions that structurally embed these elements into their plans from inception will have the strongest applications and the highest probability of obtaining the full 30% credit.

THE TWO-CERTIFICATE PROCESS

The EFICA operates through a sequential two-certificate process managed by a Technical Committee (chaired by SHCP’s Undersecretary of Revenue, with IMCINE as voting member and the Secretaría de Cultura in an advisory role):

Certificate 1: Constancia de Presentación de Trámite (Filing Certificate)

- Filed during pre-production or shooting (for productions) or before commencement (for post-production processes).

- Requires: tax compliance opinion, project description, budget, script/synopsis, production plan, creative direction proposal, and supplier contracts or letters of intent covering at least 50% of eligible expenditures.

- Timeline: Secretarial review (10 business days) → Cure period if needed (5+3 business days) → Referral to IMCINE (5 business days) → Committee session (15 business days) → Notification (5 business days). Total estimated: ~40 business days from complete filing.

- Negative fiction: If no certificate is issued within the notification period, the request is deemed denied. This is an aggressive timeline—applicants should prepare thoroughly before filing.

Certificate 2: Constancia de Cumplimiento (Compliance Certificate)

- Filed after the production is completed.

- Key requirement: An independent CPI (Registered Public Accountant) report certifying total project cost, that at least 70% of supply chain is national, that expenditures are deductible and properly documented, and the credit allocation among transferees.

- On-screen acknowledgment of the Government of Mexico incentive must appear in the final credits.

- The Compliance Certificate is valid through 30 September 2030.

- Transfers must be executed within the same fiscal year the Compliance Certificate is issued.

ELIGIBLE AND NON-ELIGIBLE EXPENDITURES: KEY HIGHLIGHTS

The Guidelines include an exhaustive Annex that classifies expenses into three categories: Direct Eligible, Indirect Eligible, and Non-Eligible. The level of detail is unprecedented for a Mexican tax incentive—covering over 120 specific line items from script development through IMF delivery for streaming platforms.

Notable Inclusions

- AI-assisted upscaling is expressly listed as an eligible expense, signaling openness to emerging production technologies.

- Intimacy coordinators and safety officers are included—reflecting alignment with international production standards.

- Cloud storage for production assets is eligible as an indirect expense.

- Audiodescription and multilingual subtitling are eligible, supporting accessibility and global distribution.

Critical Exclusions

- VAT (IVA) is not eligible —only the net cost (before tax) counts. Since IVA is creditable, this is logical but must be factored into budget projections.

- Fixed asset purchases are excluded; only equipment rentals qualify. Productions must lease, not buy.

- Corporate overhead, general accounting, and non-project office expenses do not qualify.

- Payments between related parties that are not at arm’s length are excluded.

- Cash payments not meeting fiscal documentation rules are excluded, all credit transfer payments must be via wire, check, or card.

- Salaries of the applicant’s own employees working on the project are expressly non-eligible. This is an important trap: productions must structure crew engagement through independent service agreements, not payroll.

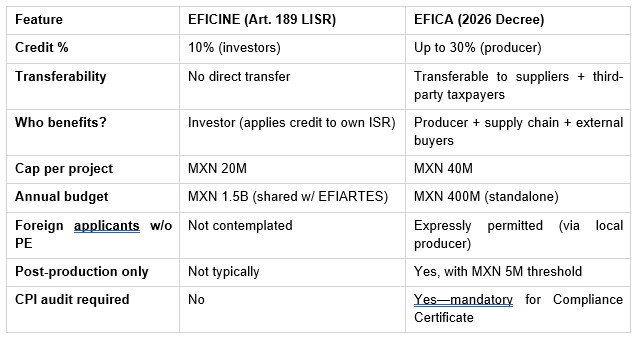

EFICA VS. EFICINE: A STRUCTURAL SHIFT

The Decree explicitly provides that applicants who are already using the EFICINE stimulus under Article 189 of the Income Tax Law for the same project cannot also apply for EFICA. However, the two programs differ fundamentally:

REVOCATION AND COMPLIANCE RISK

The Guidelines establish a formal revocation process with significant consequences:

- Certificates can be revoked if information is found to be false, if the applicant falls into an exclusion case (Articles 69, 69-B, 69-B Bis CFF blacklists), or if the project deviates from the approved parameters.

- If revoked, all beneficiaries—the producer, national suppliers, and third-party credit buyers—must file amended returns and repay the credited ISR with inflation adjustments (actualización) and surcharges (recargos) within one month of notification.

- Lifetime ban: A revoked applicant is permanently barred from future EFICA applications. There is no second chance.

- Joint and several liability: National suppliers and third-party credit buyers who voluntarily declare solidarity with the applicant assume repayment exposure if the certificate is revoked.

Practical insight: Credit buyers should conduct thorough due diligence on the production and the producer before purchasing EFICA credits. The joint liability mechanism means a credit buyer’s tax benefit is only as solid as the producer’s compliance.

STRATEGIC CONSIDERATIONS BY CLIENT TYPE

For International Studios and Streamers

- EFICA’s explicit accommodation of foreign residents without PE, operating through a Mexican service producer, provides a clean structure for runaway productions.

- The requirement of a formal co-production agreement (with IMCINE’s prior recognition for international co-productions) should be factored into deal timelines.

- Combined with Mexico’s competitive crew rates, the 30% credit on post-production alone could shift VFX and finishing work southward.

For Mexican Production Companies

- The credit is a powerful tool to reduce effective production costs by up to 30%—but the compliance burden is significant. Engaging a CPI from the outset, maintaining rigorous CFDI documentation, and mapping the supply chain to meet the 70% national threshold are essential.

- For companies without sufficient ISR liability to absorb the credit, the transfer mechanism to third-party taxpayers at up to 85% of face value effectively monetizes the incentive.

For Corporate Tax Departments and Investment Funds

- Purchasing EFICA credits at a 15% discount is economically attractive but requires careful structuring: the credit cannot exceed 15% of the buyer’s fiscal profit, payments must be via electronic transfer or nominated check, and the purchase must be formalized in a detailed contract post-Compliance Certificate.

- This creates an emerging asset class in Mexico’s tax ecosystem. Expect intermediation and brokerage activity to develop around EFICA credit transfers.

For Legal and Tax Advisors

- The requirement for all transfer documents to be submitted at the Filing Certificate stage means deal structures must be defined early—not after wrap.

- The Guidelines mandate that credit transfer contracts include an express non-retransfer clause. Advise clients that any attempt to structure secondary transfers (including through reorganizations) will jeopardize the entire credit.

RECOMMENDED NEXT STEPS

- Audit existing and planned productions for EFICA eligibility. Focus on the minimum spend thresholds and the 70% national supply chain requirement.

- Engage a Registered Public Accountant (CPI) early to structure the financial reporting framework the Compliance Certificate will require.

- Map your vendor ecosystem against the Annex’s eligible expense taxonomy and secure contracts or letters of intent covering at least 50% of the budget before filing.

- If planning to transfer credits, identify potential buyers now. The transfer structure, pricing, and buyer’s fiscal profile must be disclosed at the Filing Certificate stage.

- For international co-productions, obtain IMCINE’s prior co-production recognition before filing the EFICA application.

- Act promptly: The annual MXN 400 million budget is a hard cap. The program will operate on a first-come, first-served basis within each Committee session cycle. Early movers will capture a disproportionate share of the available credits.

For additional information, please contact:

Sergio Legorreta at [email protected] with any questions or more specific situations.

FisherBroyles is an international law firm practicing in a number of jurisdictions both in the United States and overseas through affiliated legal entities and branch offices of those entities. Legal services in Mexico are provided through Bravo Gutierrez & Münch, S.C., a member of FisherBroyles (the “Contracting Member”), with offices located in Mexico City, at Parque Lincoln, 5th Floor, Aristoteles 77, Polanco, Mexico City, Ciudad de Mexico 11560 and in Monterrey, at Blvd. Antonio L. Rodriguez 3000-5to piso Interior, 501 Torre Albia, Col. Santa Maria 64650 Monterrey, N.L.

The FisherBroyles Members engage in coordinated international legal practice and may share certain support services but are separate legal entities, each of which is solely responsible for its own work and is not responsible for the work of any other FisherBroyles Member. Each FisherBroyles Member is subject to the laws and regulations of the particular jurisdiction or jurisdictions in which it operates. Full details of the legal and regulatory status of each FisherBroyles Member are available on the FisherBroyles website.

The use of the name FisherBroyles is for description purposes only and does not imply that the Member Firms are in a partnership or are part of an LLP. The use of the word “partner” on any Member Firm’s website or in any other Member Firm materials refers to a partner or member of a FisherBroyles Member or an employee or consultant with equivalent standing and qualifications. You agree that your relationship is with the Contracting Member and not with another FisherBroyles Member unless otherwise confirmed in writing to you. You also agree that your relationship is not with any individual who is a member, employee, or consultant (including anyone we call a partner) of the Contracting Firm Member, who will therefore assume, to the extent permitted by law, no personal liability to you. Absent the explicit agreement and consent of both entities involved, no FisherBroyles Member is responsible for the acts or omissions of, nor has any authority to obligate or otherwise bind, any other FisherBroyles Member.

About FisherBroyles, LLP

Founded in 2002, FisherBroyles, LLP is the first and one of the world’s largest distributed law firm partnerships. The Next Generation Law Firm® has grown to hundreds of partners practicing in 32 markets globally. The FisherBroyles’ efficient and cost-effective Law Firm 2.0® model leverages talent and technology instead of unnecessary overhead that does not add value to our clients, all without sacrificing BigLaw quality. Visit our website at www.fisherbroyles.com to learn more about our firm’s unique approach and how we can best meet your legal needs.

These materials have been prepared for informational purposes only, do not constitute legal advice, and under applicable rules of professional conduct governing attorneys in various jurisdictions, may be considered advertising materials. This information is not intended to and does not create an attorney-client or similar relationship. Whether you need legal services and which lawyer you select are important decisions that should not be based on these materials and information alone.

© 2026 FisherBroyles, LLP